By 2023, the global AI market size had already hit about $197.5 billion. Analysts are calling for a 37% compound annual growth rate through 2030, one of the highest CAGR figures among tech markets. Numbers like that are hard to brush aside. But those charts don’t answer the real questions: When should you invest, how much should you commit, and what return can you count on?

Here's where Aloa steps in. We help you turn AI projections into working results, whether that means spinning up a rapid prototype or building custom AI tuned to your industry. Start small, prove the value, then scale. That way, you’re not burning through budget chasing hype.

But quick wins are only half the story. The trillion-dollar artificial intelligence market is being pulled by three big forces:

- Enterprise Adoption

- Infrastructure Expansion

- Regulatory Evolution

We’ll talk through how these create opportunities, where the risks are hiding, and how to line up your strategy so it actually works.

What Is the Market Size of the AI Industry in 2025?

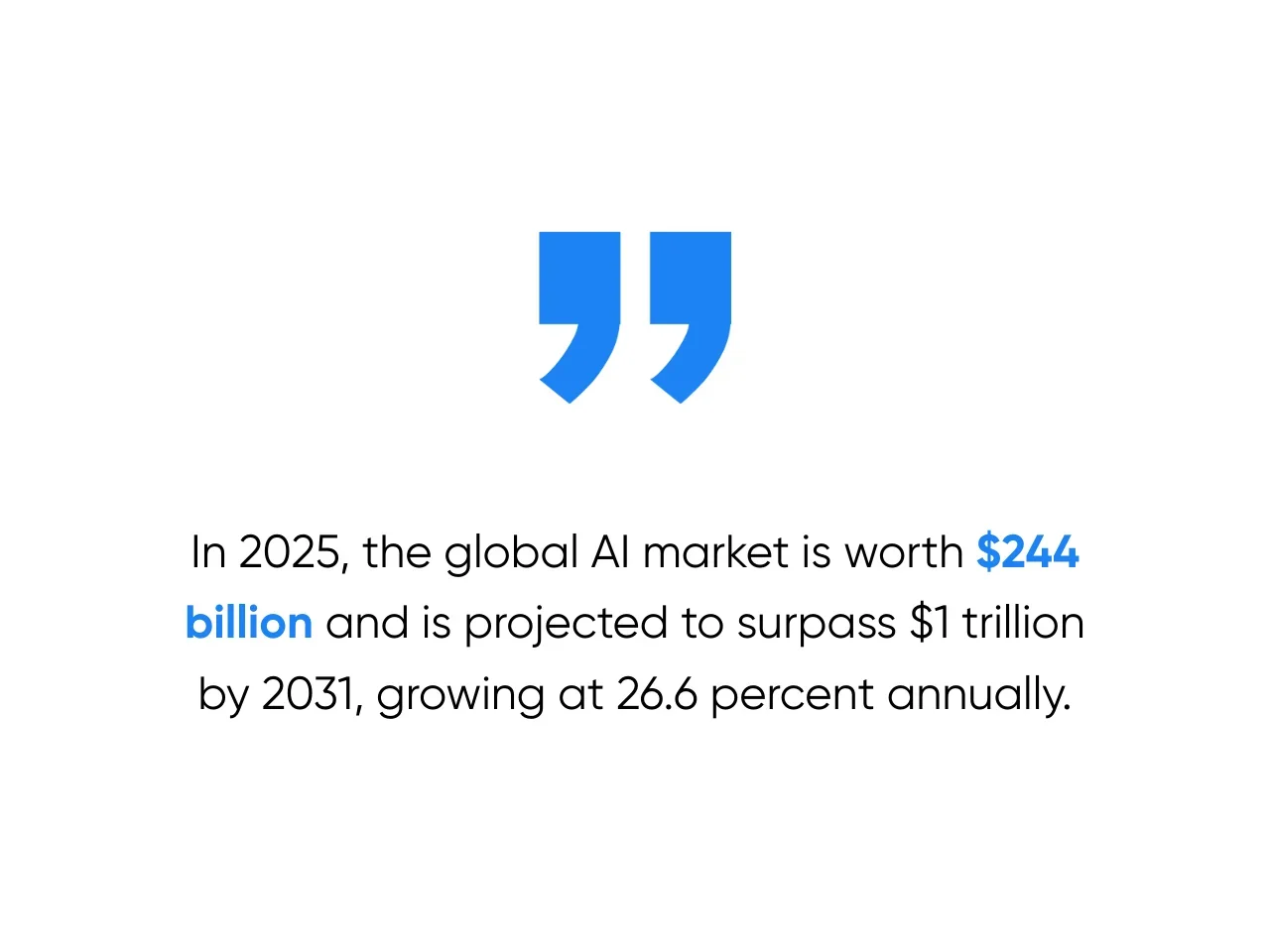

In 2025, the global AI market size sits around $244 billion. Projections say it could climb past $1 trillion by 2031, growing at about 26.6% a year. Put simply, AI is set to more than quadruple in just six years. It’s hard to ignore how quickly AI is scaling.

When we look under the hood, this surge is being pushed by three main forces: how fast enterprises adopt AI, the infrastructure that makes it run, and the regulations that shape its use. Keep those in mind, because they’re the real story behind the trillion-dollar projections we’ll unpack next.

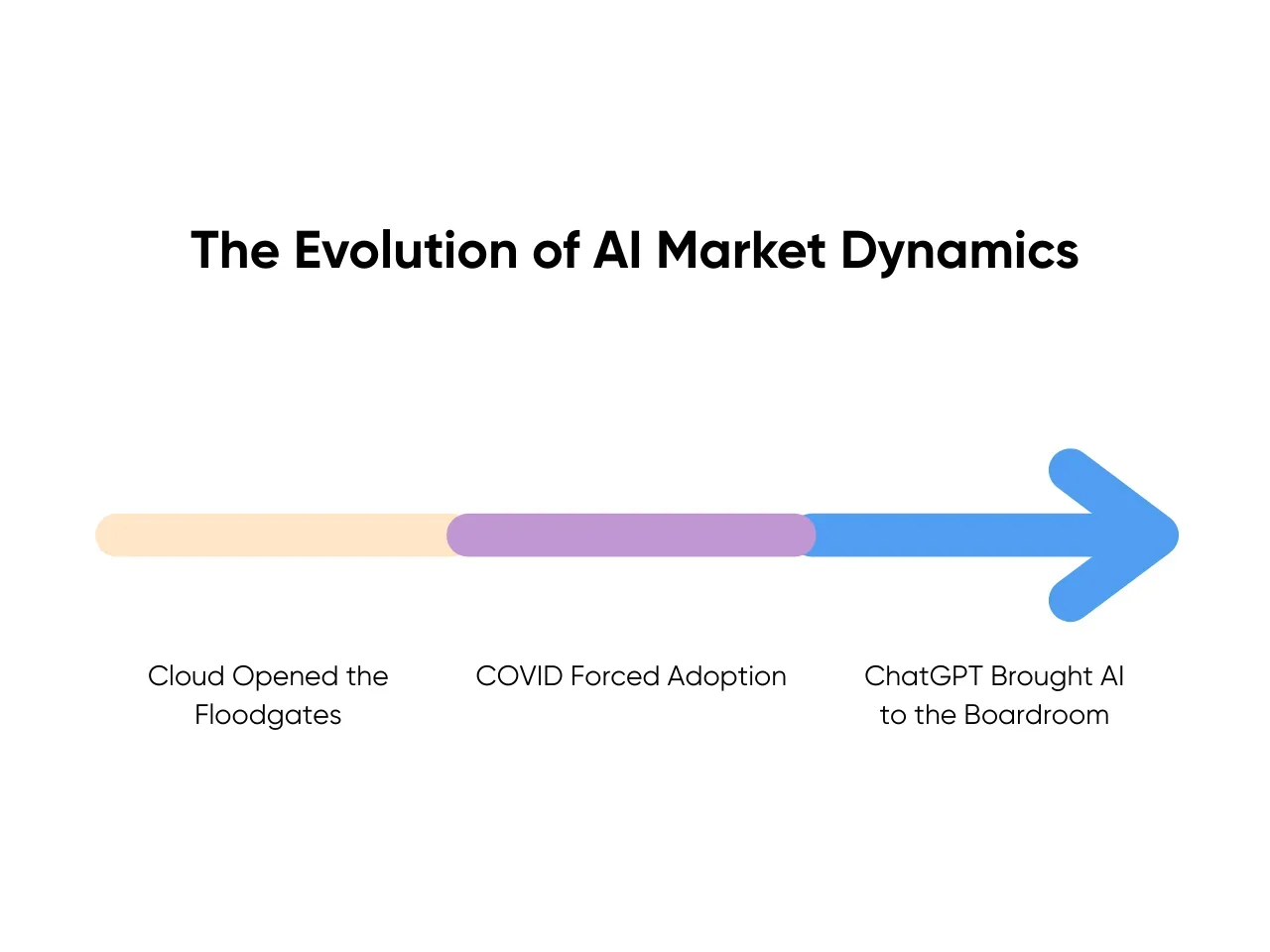

The Evolution of AI Market Dynamics

The AI market practically leaped forward in bursts. In 2019, the industry was worth around $40–50 billion. By the end of 2023, it had ballooned to nearly $200 billion, with 2024 estimates ranging between $184 and $279 billion depending on who you ask. That’s not organic drift, but accelerants hitting the system.

Market Size Trajectory

Consider these three accelerants in particular:

- Cloud opened the floodgates: Once AWS, Azure, and Google Cloud made AI tools available as on-demand services, mid-sized companies suddenly had access to machine learning capabilities that used to require in-house servers, data scientists, and research institutes. For the first time, a midsize retailer or logistics firm could run predictive analytics without a huge IT budget.

- COVID forced adoption: The pandemic made AI less of a “nice to have.” Walmart leaned on AI to forecast demand when shelves were empty, while FedEx used algorithms to keep routes efficient as delivery volume spiked. In recent years, survival, not strategy, has pushed the adoption of AI across various industries.

- ChatGPT made AI impossible to ignore: Its late-2022 release was a watershed moment. Suddenly, HR managers were testing job descriptions, legal teams were asking about contract summaries, and executives couldn’t ignore the use of AI in everyday workflows. This wasn’t abstract research anymore. It was artificial intelligence in the hands of regular staff with natural language, speech recognition, and even early computer vision use cases showing up.

That’s the pattern: adoption accelerates when barriers to access drop, or when delay becomes too costly. In other words, market growth is about forecasts and pressure points that force real-world implementation of AI.

Technological Breakthroughs

Here’s where the story gets interesting. The artificial intelligence market didn’t just expand because of hype. It grew because breakthroughs solved real business bottlenecks.

- Generative AI at scale: GPT-5 just launched in August 2025, and early adopters are already testing its potential. OpenAI reports it makes about 45% fewer factual errors than GPT-4o. Even with the previous model, Morgan Stanley advisors use a GPT-4-powered assistant to scan 100,000+ research reports instantly, which cuts manual review from hours to minutes. That’s the kind of ROI enterprises hope GPT-5 can expand on in the months ahead.

- AI copilots for developers: GitHub Copilot didn’t just make coding “easier.” Studies show developers completed tasks up to 55% faster. Faster coding means faster features, earlier releases, and quicker revenue recognition. In software engineering and computer science, time really is money.

- AI agents in customer service: Airlines like Delta now deploy AI assistants that guide travelers through details like passport reminders, gate directions, and security updates. Not a full replacement for human agents, but enough to cut routine questions before they ever hit call centers. The payoff? Shorter queues, lighter staff loads, and better customer experience with a positive impact on both efficiency and trust.

This is exactly why we provide generative AI services at Aloa. You need safe ways to test tools in order to take advantage of these technological advances.

And let’s be blunt: many attempts at AI integration tend to fail at first. Companies that chase headlines without adopting AI thoughtfully can easily walk away with nothing but sunk costs. The winners are the ones who tie experiments to metrics that we actually care about: savings, revenue lift, and customer engagement.

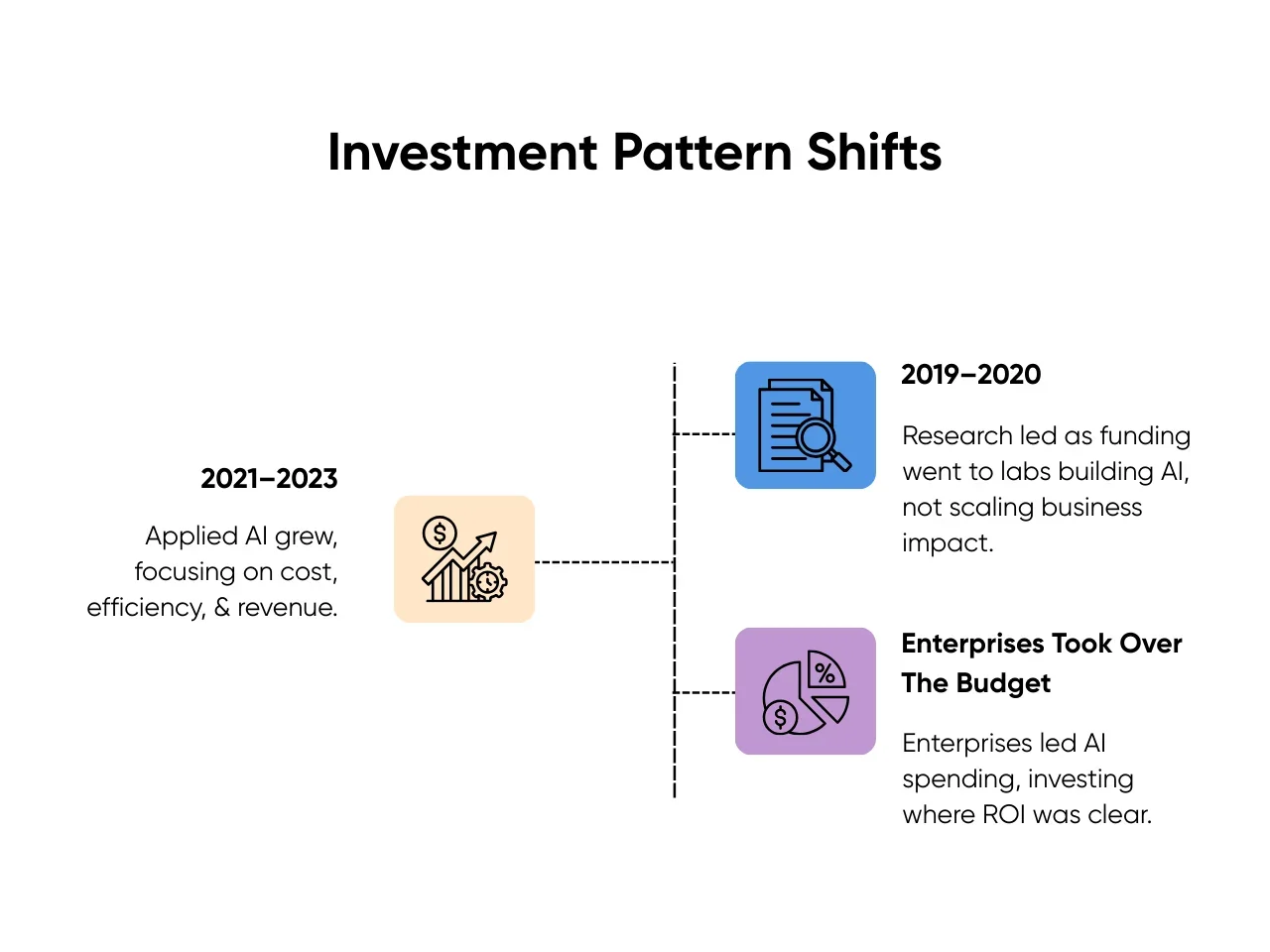

Investment Pattern Shifts

Follow the money, and the story of the artificial intelligence market becomes even clearer. In recent years, capital flows have shifted sharply, from research-heavy bets to applied use cases driving measurable ROI:

- 2019–2020: Research dominated. Most funding went into AI research, with labs and research institutions exploring deep learning and big data applications. These investments were about building AI capabilities, not yet about scaling business impact.

- 2021–2023: Applied AI took the lead. Fueled by demand for process automation in heavy industry and logistics, dollars started chasing fraud detection in banking, recommendation engines in retail, and predictive maintenance in manufacturing. In other words, AI development that cut costs, boosted efficiency, and drove revenue in various industries.

- Enterprises took over the budget: JPMorgan alone set aside billions for AI in trading and risk management. Meanwhile, mid-sized manufacturers were quietly investing in predictive analytics to cut equipment downtime. Whether in financial services or factory floors, the pattern was the same: adoption of AI where ROI was clearest.

That shift is exactly why we’ve doubled down on internal tooling and workflow automation at Aloa. Our AI solutions help companies streamline processes, reduce operating costs, and implement the kind of ROI-driven use cases your team is asking for.

Here’s the bigger picture: McKinsey estimates that fully implemented generative AI could add $2.6 to $4.4 trillion annually to the global economy. That’s potential, not a guarantee. Which is why the next three growth drivers matter. They’re the lens that separates sustainable market growth from risky bets.

Core Market Growth Driver #1: Enterprise AI Adoption

If you’re wondering where most of the fuel for the AI market size comes from, the short answer is simple: enterprises. Leaders might argue over when to jump in, but hardly anyone’s still questioning whether AI is optional. When a peer bank is reporting sharp drops in fraud losses or a retailer is lifting sales with personalization engines, waiting suddenly looks like the bigger risk.

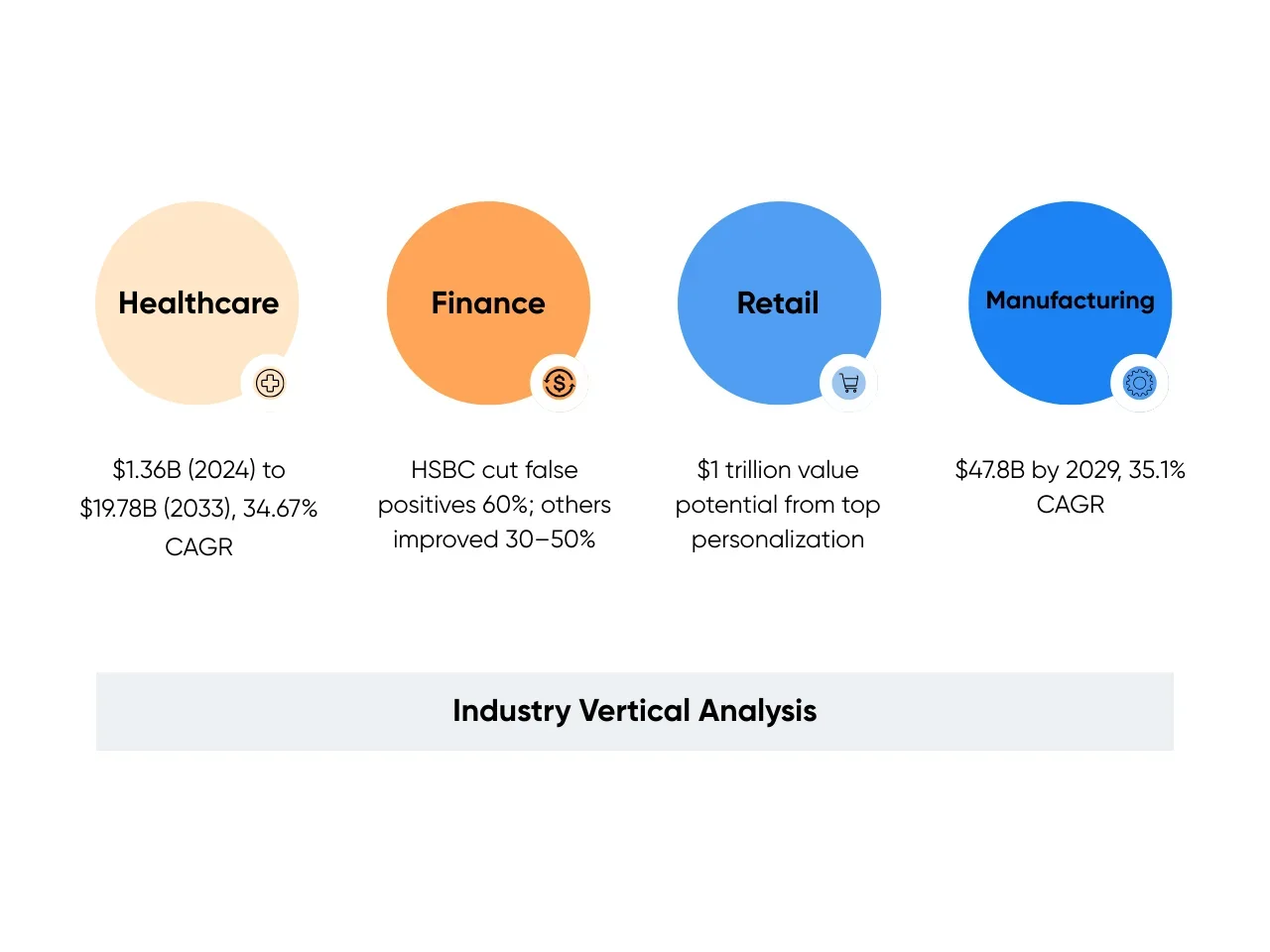

Industry Vertical Analysis

Enterprise adoption doesn’t look the same everywhere. But the throughline is impact that ties back to the bottom line:

- Healthcare: The global AI in medical imaging market was about $1.36 billion in 2024 and could reach $19.78 billion by 2033, growing at a 34.67% CAGR. Hospitals are already piloting AI-powered image processing tools combining computer vision with other technological innovations to improve accuracy. Early detection not only saves lives but also reduces costly late interventions.

- Finance: Machine learning has proven most effective in fraud detection. HSBC cut false positives by 60% after deploying AI algorithms, while other banks report 30–50% improvements in fraud identification and loss reduction. In an industry where customer experience is everything, fewer false alarms mean both savings and trust.

- Retail: McKinsey estimates that moving personalization performance to the top quartile could unlock $1 trillion in additional value across US industries. Retailers using AI-driven recommendation engines are already seeing double-digit lifts in return on ad spend and retention, which translates directly into millions in annual revenue.

- Manufacturing: Predictive maintenance has shifted from experiment to clear use cases for process automation on the factory floor. MarketsandMarkets also projects the global predictive maintenance market to hit $47.8 billion by 2029 at a 35.1% CAGR. For a mid-sized manufacturer, even a modest 5–10% downtime reduction could mean six-figure annual savings per plant.

Not every rollout is smooth. Healthcare AI projects often stall on data quality, and personalization in retail can backfire if tuned poorly. But the companies that win aren’t the ones who avoid setbacks. They’re the ones who refine, retest, and double down where the ROI is strongest.

Implementation Priorities

Once leaders agree AI isn’t optional, the next question is: where do we start? In practice, the smartest entry points are projects that deliver visible returns with manageable risk:

- Workflow Automation: Expense approvals, invoice matching, and compliance reporting are repetitive, low-value tasks that are perfect for AI-driven automation. Enterprises report cutting approval cycle times by 30–50%, freeing up thousands of staff hours annually. That’s the capacity you can redirect to higher-value work.

- Natural Language Processing (NLP): Chatbots have evolved beyond FAQs. Trained on full workflows, they can reset passwords, file claims, and even process cancellations. One telecom company reported its AI assistant resolved more than half of inquiries without human escalation, cutting live-agent load by 70%. For support teams, that means fewer midnight calls and less burnout.

- Predictive Analytics: Retailers are using predictive models to anticipate demand swings and adjust inventory ahead of time. Churn prediction works the same way: AI can flag which customers are at risk so retention offers hit at the right moment. Studies show proactive retention can boost customer loyalty by 10–20% while cutting excess inventory costs. In plain terms, you sell more of what you stock and lose fewer customers along the way.

- AI Agents: In procurement, they can vet suppliers, negotiate terms, and draft contracts far faster than human teams alone. In sales, they act as virtual assistants that qualify leads, schedule demos, and send follow-ups automatically. For many companies, this has shortened sales cycles from months to weeks, accelerating both cash flow and revenue recognition.

Some executives worry these early pilots won’t scale fast enough. But pilots aren’t about transforming the whole company overnight. They’re about building momentum. Trim approval times in half or cut customer support queues in minutes, and suddenly you’ve got the proof (and political capital) to pitch bigger initiatives.

ROI & Success Metrics

At the end of the day, AI adoption only sticks when it delivers numbers you and your leadership team care about. It’s not enough to say a project “worked.” You need to connect it to hard KPIs, like savings, revenue lift, or customer retention.

- Personalization ROI: McKinsey estimates personalization leaders could unlock $1 trillion in incremental value. For retailers, that plays out as 10–20% lifts in repeat purchases and millions in lifetime customer value.

- Fraud Detection ROI: Banks using AI-powered fraud detection report 30–50% loss reductions. HSBC saw a 60% drop in false positives alone. The payoff is fewer customers locked out of accounts and millions saved in avoided chargebacks.

- Predictive Maintenance ROI: MarketsandMarkets projects predictive maintenance to reach $47.8 billion by 2029, because the economics are proven. Just a 10% downtime cut can save mid-sized manufacturers hundreds of thousands annually per plant. Scale that across multiple sites, and the savings stack fast.

This is the kind of ROI case that turns AI from a “technology experiment” into a budget priority. And it’s why at Aloa, we design pilots with KPIs baked in from the start. That way, you’re not defending AI as a trend. You’re presenting it as a line item with measurable return.

Core Market Growth Driver #2: AI Infrastructure Expansion

If adoption is the fuel, infrastructure is the engine. Fraud detection, copilots, and chatbots all sound great on slides and strategy talks. But to make them work across an enterprise, you need horsepower: GPUs to train models, databases to ground them, and pipelines to deploy them reliably. Without that, even the smartest pilots stall.

Here’s the bottom line: the trillion-dollar AI market size is happening because the infrastructure is (slowly) catching up. When compute and storage are in place, companies can move pilots into production without breaking budgets (or breaking trust). That’s when the market expands: when AI stops being a test case and becomes part of daily operations.

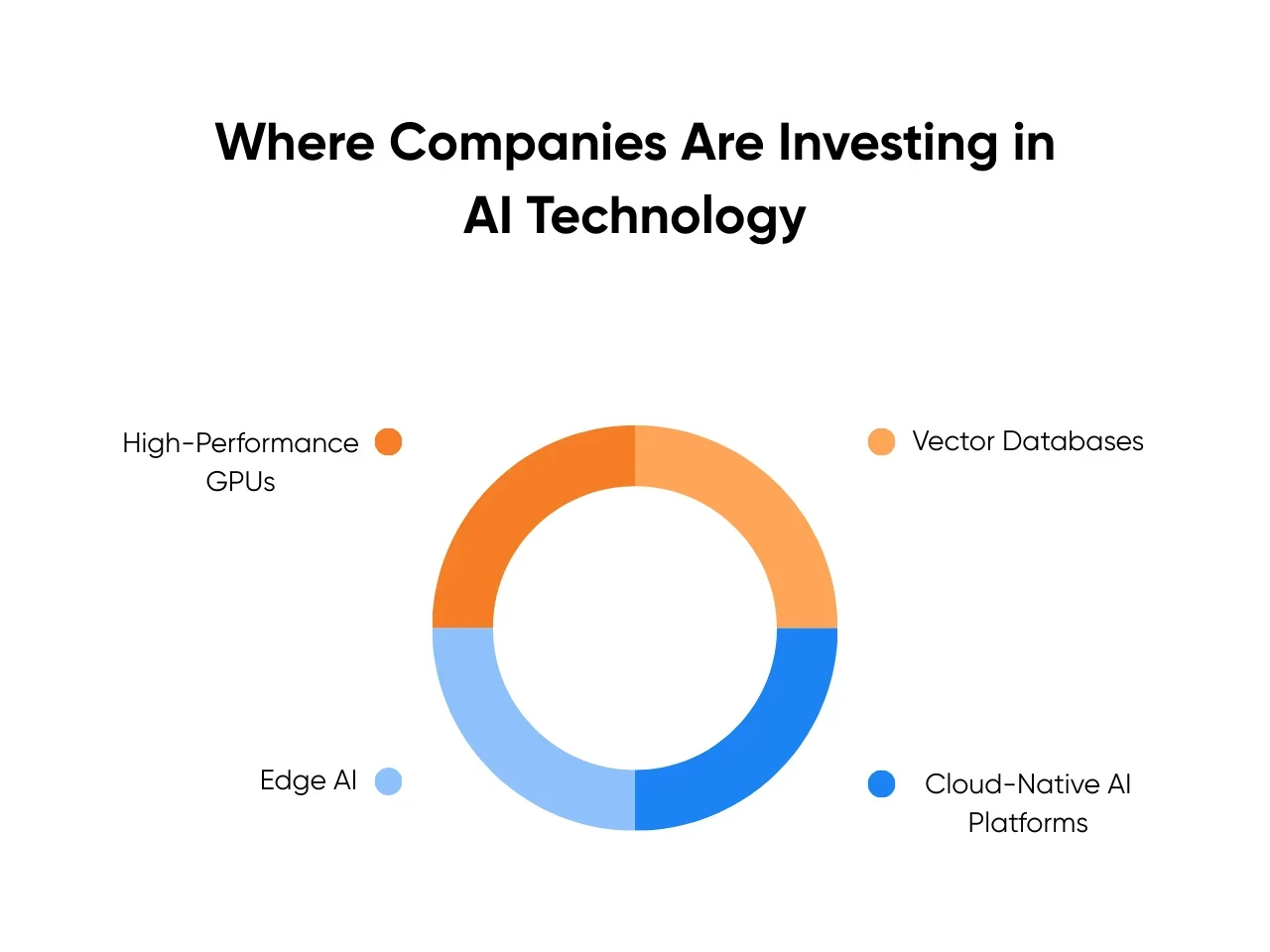

Where the Money Is Going

So, where are companies actually writing checks? Four areas stand out:

- High-Performance GPUs: NVIDIA’s data center revenue hit $47.5B in 2024, up more than 400% in a year. The demand came from hospitals training imaging models, banks fine-tuning fraud detection, and tech giants scaling generative AI, especially across North America and the Asia Pacific. So, if you’re planning AI development at scale, don’t wait until you need GPUs. Secure access early through cloud credits, partnerships, or advance contracts. Delays of even a few months can set your rollout back.

- Vector Databases: Think of these as the memory banks for AI. They make retrieval-augmented generation (RAG) possible, grounding outputs in your own data instead of letting models “make things up.” That’s why vector database companies like Pinecone, Milvus, and Weaviate are securing significant funding. Practical move? Start small. Index contracts, support docs, or a product catalog. Prove that the model can answer your questions before trying to boil the ocean.

- Cloud-Native AI Platforms: AWS Bedrock, Azure OpenAI, and Google Vertex AI let mid-sized firms rent access to powerful models through APIs. No massive machine learning team required. Logistics companies are already spinning up routing tools in weeks instead of years. If you’re a mid-sized enterprise, this is the easiest on-ramp: prototype, pay for what you use, and only scale if it sticks.

- Edge AI: Latency and privacy make this non-negotiable in some sectors. Retailers are running in-store recommendation engines locally to keep shoppers engaged in real time. Manufacturers are embedding AI cameras on production lines to catch defects before they hit shipping. Hospitals process scans inside their own networks, so sensitive data never leaves the building. If compliance or speed are deal-breakers in your industry, test edge deployments early. You’ll find out quickly whether it saves you from regulatory headaches or downtime losses.

Each of these bets chips away at friction in a different way: faster training, safer outputs, quicker deployment, or tighter compliance. Together, they turn AI from a big promise in meetings into a tool you can actually run day to day.

The Cost Catch

Of course, there’s a catch: price. Training a frontier model can run into the tens of millions. Even running inference adds up. Estimates put OpenAI’s ChatGPT compute bill at over $700K per day.

Here’s where leaders trip:

- Overbuying GPUs without a clear plan for workloads.

- Locking into multi-year cloud contracts before usage patterns are stable.

Both leave you with ballooned budgets and no flexibility. Smarter operators phase it in: start with cloud APIs, test with vector DBs on a narrow use case, then scale to edge only when latency or compliance demand it.

Looking Toward 2030

The pressure only increases from here:

- Compute Demand: By late 2027, leading AI companies are expected to be running 20–40x more training compute than in 2024. And globally available AI-relevant compute may be about 10x higher. That kind of growth compounds by 2030. So, expect supply-chain fights for GPUs and energy bills that grab the CFO’s attention. Smarter teams are planning in phases; secure capacity in chunks, not in one giant contract.

- Data Management: Most enterprises are already at 80%+ unstructured data (video, audio, documents, natural language), and those that aren’t will hit it by late 2025. Waiting until 2030 to act is a losing play. Treat vector search and scalable storage as baseline now. A practical first step? Index one high-value dataset (contracts, support docs, or a product catalog) and measure retrieval quality before you expand.

- Deployment Flexibility: Hybrid is already the default. Banks keep compliance workloads on-prem but run trading models in the cloud. Manufacturers centralize analytics but run defect detection at the edge. The actionable move is to design systems that can roll out, roll back, and burst between environments. That way, you can shift costs, handle policy changes, or respond to downtime without rewriting everything.

At Aloa, we help teams design infrastructure roadmaps that stay flexible. Some start cloud-first with tight spend monitoring. Others, especially in healthcare and manufacturing, test edge deployments early because they can’t compromise on data control.

The goal isn’t to chase the flashiest hardware. It’s to make sure every infrastructure dollar ties back to something you can point to in a board meeting: shorter rollout cycles, lower costs, or better customer experience.

Core Market Growth Driver #3: Regulatory Evolution

If adoption is the fuel and infrastructure the engine, regulation is the guardrail. It’s not flashy, but it decides how fast (and how safely) you can scale AI. For most leaders, the real debate isn’t “Can we build it?” It’s “Can we roll it out without tripping over compliance or reputational landmines?”

Why Regulation Shapes Growth

Here’s the thing: markets stall without trust. Customers hesitate if they think their data isn’t safe. Investors slow down if compliance risk feels unpredictable. Clear rules give both groups confidence to stay in the game.

But predictability has a price. Compliance reviews, model audits, and data-localization rules eat up budget. Guidance varies, but analysts suggest AI governance can consume 7–20% of total project spend depending on risk level. For a $10M rollout, that’s anywhere from hundreds of thousands to a couple million set aside for oversight before launch.

Regional Approaches

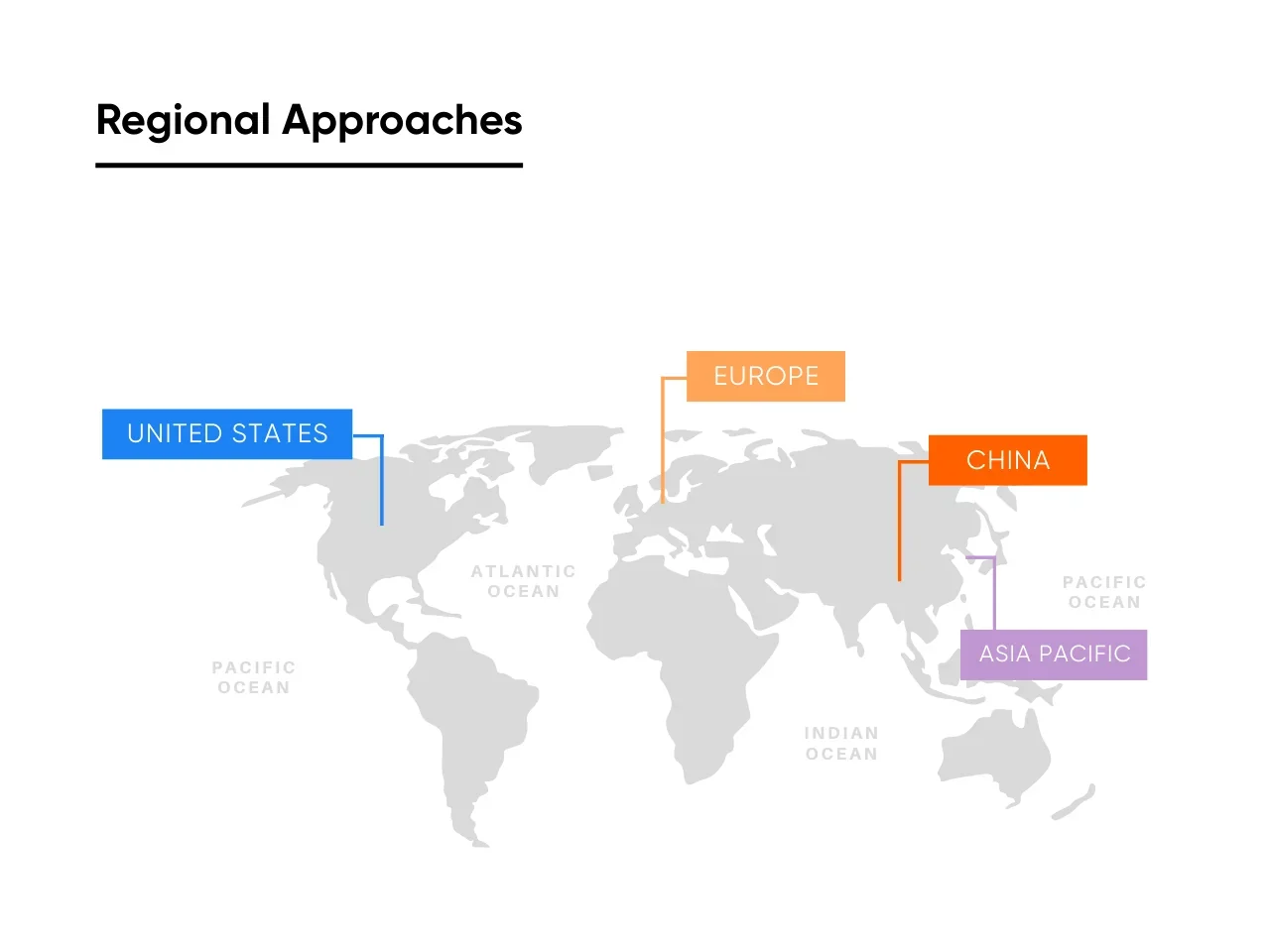

So how heavy does that load feel? Depends where you’re building:

- European Union: The EU AI Act, finalized in 2024, is the most comprehensive framework yet. High-risk systems (biometric ID, credit scoring, medical devices) need formal conformity assessments. If you’re selling into Europe, audits will soon feel as routine as financial ones.

- United States: Lighter touch so far. The 2023 Executive Order set fairness and safety guidelines but left enforcement to agencies. That means faster launches today, but more uncertainty tomorrow. Firms already adding explainability features are basically buying insurance against tighter rules later.

- China: Regulators are strict, especially on generative AI. Providers must pass security checks and align outputs with state guidelines. For multinationals, that often means running parallel tracks: one system for China, another for the rest of the world.

- Asia-Pacific Hubs: South Korea announced nearly $7B in AI investment by 2027 focused on semiconductor competitiveness, especially AI chips, while Singapore and the UAE lean on lighter oversight paired with financial incentives. These regions often provide clearer regulatory signals and, in some cases, subsidies that can offset adoption costs.

Global spend on AI governance and compliance software is projected anywhere from $1.2–1.4B by 2030 on the low end to $15.8B by 2030 on the high end, depending on how broadly you define the category. Either way, it’s a market growing quickly, led by Europe but spreading across the Asia-Pacific. Even if you’re not directly in those regions, expect requirements to creep into vendor contracts.

Opportunity vs. Risk

Strong regulation isn’t always a brake. It can actually speed adoption. A hospital is more willing to use AI diagnostics when patients know the model was certified. A bank is more confident rolling out fraud detection tools if regulators stamp them as compliant.

But the flip side is cost. Preparing for audits, building transparency, and hiring compliance specialists all add up. Launching without that readiness is how mid-sized firms get burned, with fines, wasted spend, and reputational hits that stick around.

So how do you stay ahead without turning into a compliance lawyer? A few practical moves:

- Map regulations to use cases: Don’t treat compliance as one bucket. The risk level depends on whether your AI touches customer data, lending, or hiring. In Europe, audits for these categories can take 6–12 months and run $250K–$500K per project.

- Bake compliance into pilots: Retrofitting transparency after launch costs 3–5x more. Build explainability and audit readiness from day one. It’s cheaper and smoother.

- Balance markets with strategy: Europe demands heavier compliance. Asia-Pacific hubs may soften rules with incentives, sometimes covering up to 20% of rollout costs. Where you expand determines both your stack and your runway.

At Aloa, we help firms pilot with compliance built in, using explainability tools, privacy safeguards, and infrastructure tuned for audits. That could cut an EU audit timeline from nearly two years to under 12 months. Or clear the bar for Singapore’s AI incentives, trimming millions off your rollout.

The point? Compliance doesn’t have to slow you down. Done right, it’s the evidence that wins contracts and keeps your team backing the rollout.

Strategic Investment Implications

By now, the pattern’s clear: enterprises fuel adoption, infrastructure scales it, and regulation sets the guardrails. The question leaders wrestle with isn’t if to invest; it’s when, how much, and in what order. And when the order’s wrong, you don’t just waste money. You risk losing credibility with your own team and the investors.

Here’s how to frame AI investment decisions so they hold up under scrutiny:

Timing: Phased Adoption vs. Bold Bets

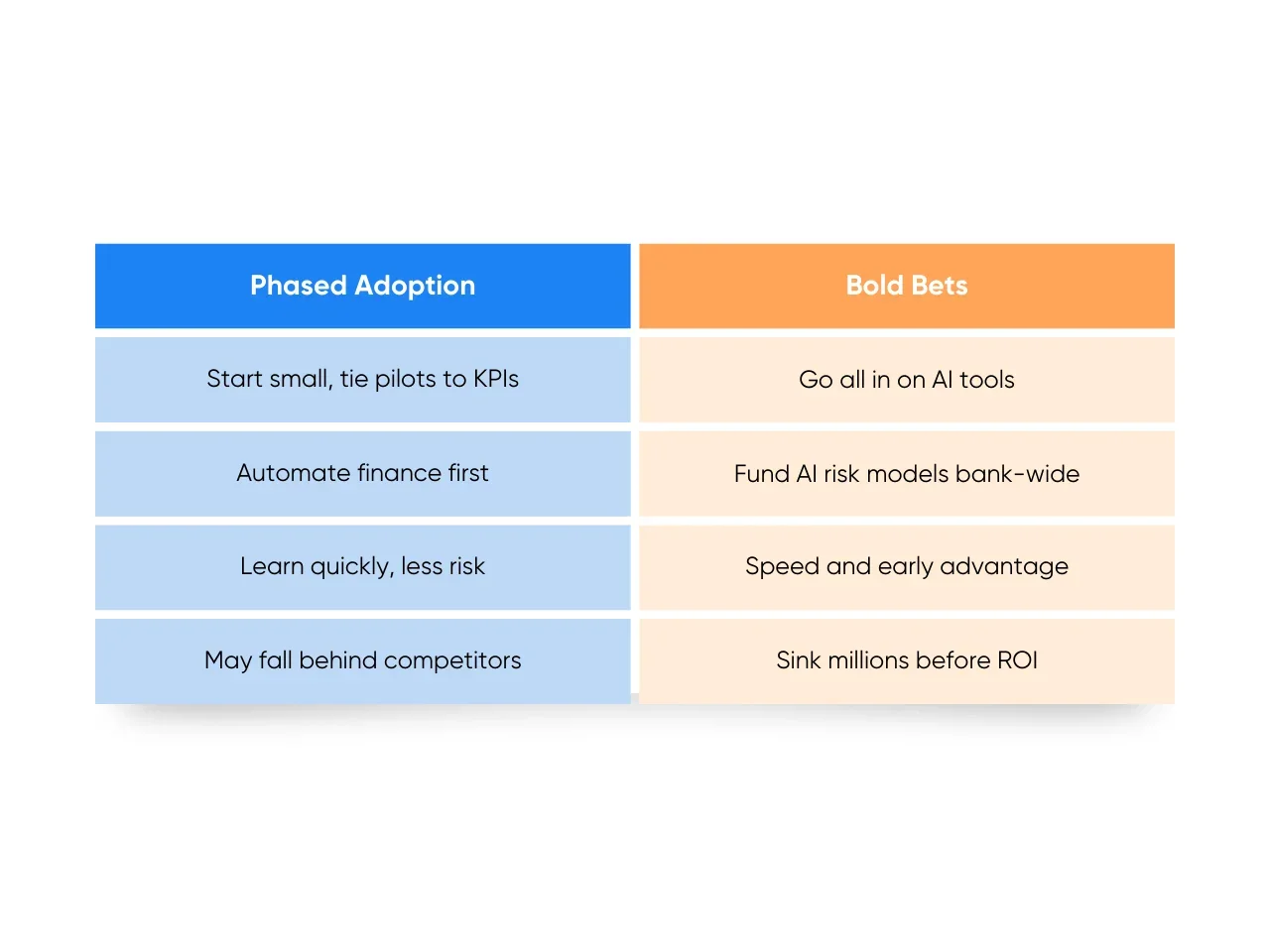

Decision-makers usually split into two camps: jump in early to get ahead, or hold back until the proof is solid. Both can work, but only if expectations are set up front:

- Phased Adoption: Start small, tie pilots to KPIs, and scale when ROI shows up. For example, rolling out workflow automation in finance before expanding into HR and compliance. The upside is you learn fast without overcommitting. The downside is that a competitor who bets big could pass you while you’re still testing.

- Bold Bets: Go all in on infrastructure or industry-specific AI tools to pull ahead early. For example, a bank funding AI-driven risk models across all trading desks in year one. The reward is speed; the risk is sinking millions before the returns are proven.

Neither is automatically safer. The real danger is picking one approach and failing to set clear benchmarks for success.

Resource Allocation: Infra, Talent, Governance

AI budgets aren’t infinite. The leaders who win treat them like a portfolio, not a blank check:

- Infrastructure: GPUs, vector databases, and cloud spend are the backbone that lets projects scale.

- Talent: Data scientists, ML engineers, and domain experts tune models to real workflows.

- Governance: Compliance staff, legal advisors, and monitoring tools keep rollouts from being derailed by audits.

Recent benchmarks suggest mid-sized firms split AI budgets roughly 20–30% infra, 40–50% talent, 10–15% governance. Where you land depends on your goals: are you building new products, streamlining operations, or expanding into regulated markets?

Risk Mitigation: ROI, Not Hype

Plenty of firms chase shiny tools only to end up with sunk costs. The fix is deceptively simple; define ROI thresholds before you start. For example:

- Financial ROI: “This project needs to save us at least $500,000 annually to be greenlit.”

- Operational ROI: “Cycle times must shrink by 25% or more to justify scaling.”

- Customer ROI: “Retention or satisfaction scores must improve by at least 10%.”

When pilots hit these benchmarks, they earn their way to the next phase. When they don’t, you cut losses early and redirect budget. That discipline is what separates ROI from hype and ensures investments reflect true market value, not just short-term technological advancements.

At Aloa, we help firms put these frameworks into practice. We can build a rapid prototype to prove ROI before you commit seven figures to infrastructure. We can also bake compliance into your pilots from day one, so a Europe rollout doesn’t drag into an 18-month audit nightmare.

Our approach is simple: treat your AI budget like a capital investment. Every dollar should defend revenue, drive growth, or reduce risk. If it doesn’t, it’s not worth spending.

Key Takeaways

The global AI market size is on track to pass $1 trillion by 2030. We are seeing enterprises adopting at scale, infrastructure catching up, and regulations putting down the guardrails. The companies actually winning are proving ROI in diagnostics, fraud detection, personalization, and predictive maintenance, then scaling only once the backbone and compliance are ready.

If you’re looking to take advantage of this huge shift in tech, that changes the framing. AI isn’t a side project anymore, but an investment conversation. Every dollar has to tie back to revenue, cost savings, or risk reduction. Miss that connection, and your pilot dies in committee. Nail it, and you’ve got a roadmap that gets funded.

At Aloa, we can help you turn AI projections into plans you and your team can trust. That might be a 90-day prototype to validate ROI, a compliance-ready rollout in Europe, or a phased infrastructure strategy that only scales when results demand it. The common thread: every project we take on is tied to business outcomes from day one.

If you’re ready to cut through hype and build an AI roadmap that actually gets funded, give us a call.